Portfolio Recovery Associates Sued Me. The Case Was Dismissed Because They Could Not Prove the Debt.

Yes, you can defend a lawsuit by Portfolio Recovery Associates. In my case, the suit was dismissed because PRA could not authenticate the documents it relied on to prove I owed the debt. That is the short answer to the question many people type into Google after a summons lands on the doorstep.

I am a Florida trial lawyer. PRA sued me. I appeared, answered, and required proof. PRA could not lay the foundation for the records it needed to win. The case was dismissed.

This article is a field report on that case, then a plain explanation of why the same evidentiary gap shows up again and again in debt-buyer litigation. It is not a promise that your case will end the same way. It is not legal advice. It is a description of what happened in one case I defended myself, and why the pattern matters if a debt buyer has sued you. For more on consumer-side debt cases on this site, see the debt defense overview.

A note on how this article got written. I run a small AI team that handles the business side of my practice while I keep practicing law. This piece is one report from that work, informed by a YouTube video on debt collection defense (source) that I watched, partially agreed with, and wanted to ground in what actually happened in my own case.

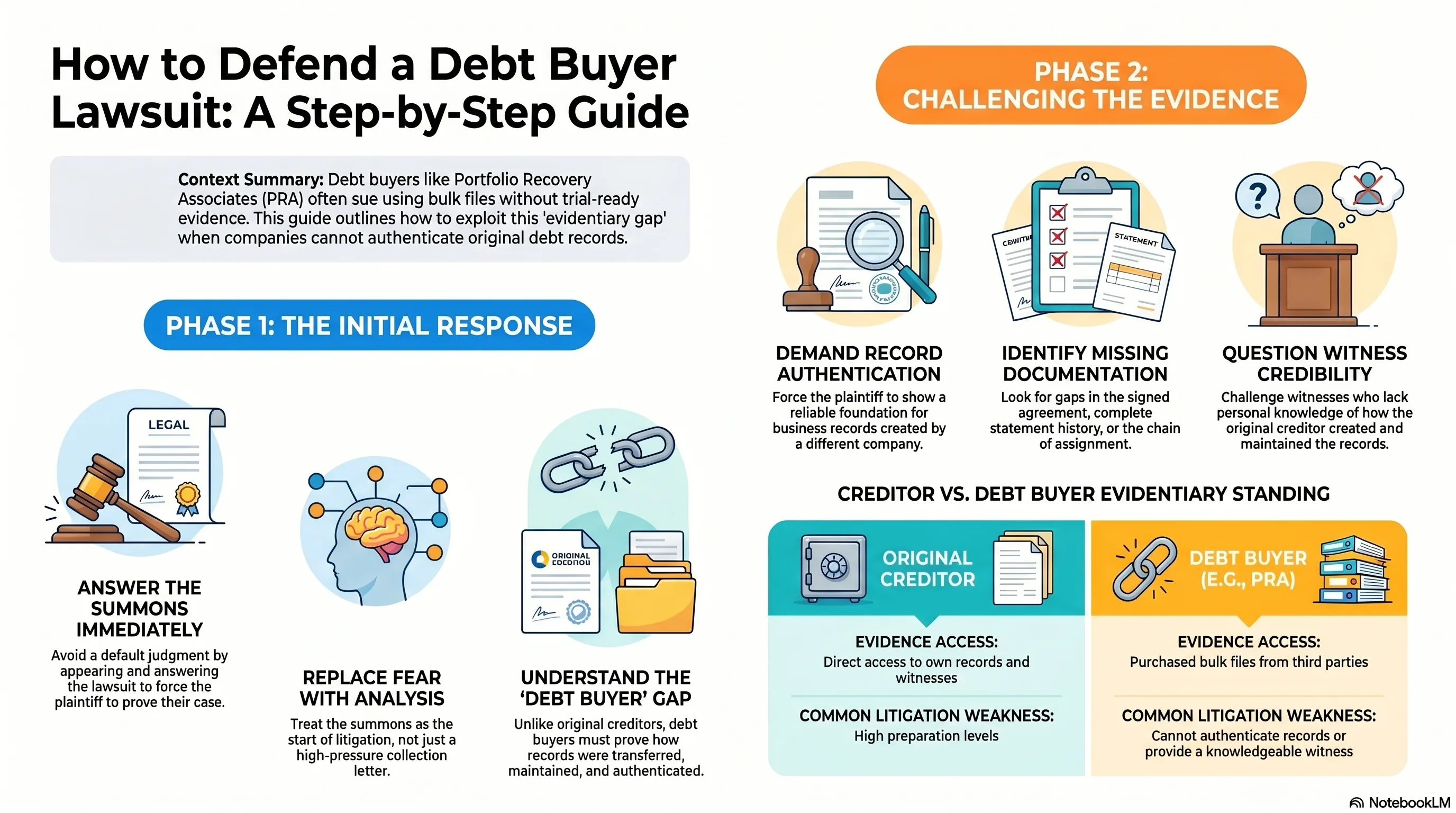

What a debt buyer is, and why that matters

A debt buyer is not the original creditor. It did not lend you money. It did not issue your card. It bought a file in bulk, usually for a small fraction of face value, after the original creditor charged the account off. Portfolio Recovery Associates is one of the largest of these companies in the country and one of the most-sued debt buyers in Florida small claims court.

This matters because of who has to prove what in court. PRA is the plaintiff. PRA carries the burden of proof. PRA has to show the account exists, that it belongs to you, that the balance is what it claims, and that the records it relies on are reliable enough for a judge to rely on too. You do not have to disprove the debt. You can sit on your hands and require PRA to prove its case the right way.

The proof problem is documents. The bulk-sale file usually contains a forward flow agreement between the original creditor and the debt buyer, some account-level data exported from the originator's systems, and an affidavit from someone at the debt buyer who says they reviewed the data. It usually does not contain the original signed agreement, the full statement history, or proof that the debt buyer's affiant has personal knowledge of how the originator's records were made.

When you appear and demand authentication of those documents, the gap shows up. That is what happened in my case.

What I did when I got served

I did not ignore it

The single biggest mistake people make is doing nothing. The default-judgment trap is real. If you ignore the summons, the court enters judgment against you for the amount sued, plus interest and costs. Most debt-buyer cases end in default. That is not because the defendants owed the debt the way the plaintiff said. It is because the defendants never showed up.

Showing up and filing an answer puts you ahead of most defendants. It does not win the case by itself. It just keeps you in the game.

I appeared and answered

I filed an answer that denied the allegations and required PRA to prove its case with admissible evidence. I did not file a flashy motion. I did not look for a magic bullet. I filed the basic pleading every defendant is entitled to file.

I demanded the original documents

This is the move that did the work. I required PRA to produce the documents that would prove I owed the debt: the original signed agreement, the full statement history, and the records that would let a custodian testify the data was reliable.

PRA produced its standard package. A forward flow agreement. Some account-level exports from the originator's systems. An affidavit from a PRA employee describing what PRA received from the seller.

It was not enough. The PRA affiant could speak to what PRA received. The PRA affiant could not speak to whether the underlying records were made accurately at the originator, in the ordinary course, by people with personal knowledge. That gap is not theoretical. It is the gap most bulk-sale files have.

The case was dismissed

The court did not adopt the records. PRA could not lay the foundation. The case was disposed of in my favor. I paid PRA nothing.

Why the same gap shows up in almost every debt-buyer case

The economics drive the document problem. Debt buyers acquire portfolios in bulk for cents on the dollar. A bulk transfer is not a careful transfer. The seller exports what is easy to export. The buyer accepts the export and resells, sues, or collects on it. Nobody in that chain is preparing for a contested trial, because almost no defendant contests.

When a defendant does contest, the buyer's affiant runs into a wall. The affiant works for the buyer. The affiant did not see the originator's bookkeeping. The affiant cannot say from personal knowledge that a charge on a statement reflects an actual purchase the consumer made, or that a balance carried forward was calculated correctly, or that the originator's records were kept in the regular course of its business.

A judge who is paying attention notices this. A defendant who knows to require it can force the issue.

What my dismissal does and does not prove

It proves that PRA could not authenticate the documents in this case, on this record, before this judge. It does not prove that every debt-buyer suit fails. It does not prove your case will end the same way. Facts differ. Documents differ. Courts differ. Judges differ. Lawyers on the other side differ.

What I learned is that the architecture of these cases favors the defendant who appears and requires proof. Most defendants do not appear. Most cases that are contested seriously enough to demand authentication run into the same foundation gap I ran into.

That is not legal advice. It is one lawyer's field report.

What I would tell someone served by a debt buyer in Florida

I cannot tell you what to do in your case. I am not your lawyer. The Florida Rules of Civil Procedure, the Florida Small Claims Rules, and the Florida Evidence Code govern these cases, and the rules vary depending on which court you got sued in. Service rules, deadlines, and discovery limits are all court-specific.

What I can describe is what worked in my case as a general pattern:

- Take the summons seriously. Read every page. Note the deadline.

- Appear. File an answer in the time the rule gives you.

- Require the plaintiff to prove its case with admissible documents. Do not concede the documents are what the plaintiff says they are.

- Pay attention to who the affiant works for. A debt buyer's employee usually cannot supply the foundation that an originator's records require.

- Some cases raise statute of limitations issues, but that is a separate analysis and depends on the facts and the law that applies.

- Be skeptical of any source promising a magic motion or a one-page fix. There is no magic motion. There is a disciplined process.

If a settlement is the right move in your case, settling can resolve the lawsuit. If you settle, the next concern is what the debt buyer reports about the account. Consumers have statutory rights to dispute information on a credit report when it is not accurate. That is not a hack. It is the ordinary rule that consumer credit reporting should be accurate. The right approach depends on the facts and what the report says.

Common mistakes I see

- Ignoring the summons. This is how most defendants lose. Appearing alone puts you ahead of most defendants.

- Treating the case as if you owe the debt because the lawsuit says you do. A complaint is an allegation. The plaintiff has to prove it.

- Looking for a buzzword fix."Standing," "chain of title," "necessary party": these are real concepts, but they are not substitutes for evidence and they will not save a case on their own. The case turns on whether the plaintiff can authenticate its records.

- Calling the debt buyer to negotiate before reading the summons. Anything you say can come back as evidence. Read the papers first.

- Assuming a "motion to dismiss" template you found online will work. Cases like these usually do not turn on a motion to dismiss. They turn on whether the plaintiff can prove the case at trial or on summary disposition.

- Hiring nobody and trusting nothing. If the math works, an attorney can be worth it. If it does not, the courts let you appear pro se. Either way, the work is the work.

Frequently asked questions

Can Portfolio Recovery Associates actually sue me in Florida?

Yes. PRA is a frequent plaintiff in Florida small claims court. Whether PRA can win against a defendant who appears and demands proof is a separate question that depends on the documents PRA has and the court's ruling on those documents.

What happens if I just ignore the lawsuit?

The court usually enters a default judgment for the plaintiff. The plaintiff can then collect on the judgment through wage garnishment, bank levy, or property liens, depending on Florida law and the defendant's circumstances. Ignoring the suit is the worst move available.

Do I need a lawyer to defend a debt-buyer case?

You can appear pro se. Many people do. Whether a lawyer is the right call depends on the amount at stake, the complexity of your case, and your own bandwidth. This article describes how I defended myself, but I am a trial lawyer. A non-lawyer defendant should at minimum read the rules that apply, know the deadlines, and be prepared to require the plaintiff to authenticate its documents.

What documents does the debt buyer need to win?

Generally, the plaintiff needs to prove the account exists, that it belongs to the defendant, that the balance is correct, and that the records relied on are reliable. In practice that means an account agreement, a statement history showing the charges and balance, charge-off and transfer records, and a witness with personal knowledge of how the originator's records were made. Missing pieces do not always kill the claim, but they often do.

What is the statute of limitations on debt-buyer cases in Florida?

Some cases raise statute of limitations issues. The applicable period depends on the type of debt, the law that governs the contract, and the facts. That is a separate analysis worth its own article.

If I settle, can I dispute the credit reporting on the account?

Consumers have statutory dispute rights when credit reporting is not accurate. The key issue is accuracy, not whether the underlying debt was originally valid. A dispute is not a lawful way to erase true information; it is a way to require the reporting to be accurate. The right approach depends on the facts of your case and what the report says.

Is this legal advice?

No. This is educational commentary describing one case I defended, and the recurring patterns I noticed. It is not legal advice and not a prediction of how any other case will turn out. Facts differ, documents differ, courts differ.

A note on what is coming

More practical guidance is coming for people defending these cases on their own. I am building an AI Debt Defense Course around the patterns I saw in my own case and others like it. There is no signup yet. When there is, it will live on this site.